How Currency Swings Affect Dubai Property Buyers in 2026

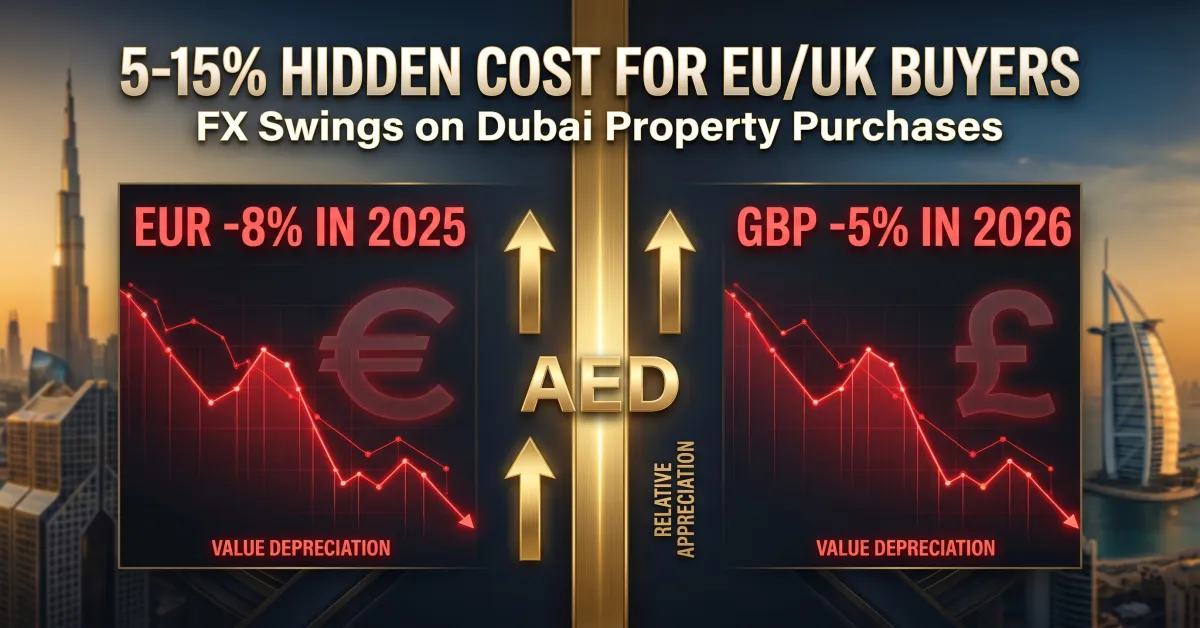

According to Early Bird Properties, the UAE Dirham has been pegged to the US Dollar at 1 USD = 3.6725 AED since November 1997, eliminating USD-side currency risk for American investors but exposing GBP, EUR, CAD, and ZAR buyers to 5-15% swings during a typical Dubai property purchase. With the euro down approximately 8% against the dollar between January and December 2025, a French buyer who committed to a Dubai property in euros at the start of 2025 paid roughly 8% more in AED terms by year-end without any change in the property's AED asking price. Understanding how currency timing affects your Dubai purchase is now as important as choosing the right area or developer.

Why the AED-USD Peg Matters for Every Dubai Property Buyer

The Central Bank of the UAE has maintained a fixed exchange rate of 1 USD = 3.6725 AED since 1997. The Central Bank intervenes automatically in the foreign exchange market, buying or selling USD to keep the dirham stable. UAE foreign exchange reserves are large enough that breaking the peg in 2026 or the foreseeable future is considered extremely unlikely.

For a US-dollar-denominated buyer, this peg is a gift: the AED price you agree on today is locked into a predictable USD figure for the entire payment timeline. There is no FX risk between contract and handover.

For non-dollar buyers, the peg works differently. Because AED moves with USD, your home currency's strength against the US dollar directly determines how expensive your Dubai property becomes. If your home currency weakens against USD between now and your final installment, the AED cost of your property rises in your home currency terms, even if the property's AED price never changes.

Quick example: A British buyer purchasing an AED 3 million property at 1 GBP = 4.6 AED pays GBP 652,174. If GBP weakens to 1 GBP = 4.4 AED before final payment, the same property now costs GBP 681,818 — a GBP 29,644 hidden increase from FX alone.

How GBP, EUR, CAD, and ZAR Move Against AED in 2026

Each major currency that funds Dubai property purchases has its own driver against the dirham. Understanding the underlying force lets buyers anticipate movement instead of reacting to headlines.

GBP — British Pound. Sterling tracks the GBP/USD pair, which is shaped by Bank of England rate decisions, UK inflation data, and oil-driven risk sentiment. In 2026, BoE has held rates as oil-fuelled inflation concerns persist, providing modest GBP strength against the euro. UK buyers benefit when sterling holds firm; weakness in GBP/USD directly raises Dubai property costs.

EUR — Euro. The euro's path to AED runs through EUR/USD. The European Central Bank cut rates faster than the Federal Reserve through 2025, contributing to an 8% EUR decline against the dollar that year. In 2026, the ECB has held rates while flagging oil-driven inflation, but eurozone growth concerns remain. European buyers face the largest sustained FX exposure of any major Dubai investor segment.

CAD — Canadian Dollar. CAD is heavily oil-correlated. With oil up over 8% during recent geopolitical escalation, the Canadian dollar gained ground, improving CAD-denominated buying power for Dubai property. Canadian investors should watch oil prices as a leading indicator of their AED purchasing strength.

ZAR — South African Rand. The rand tracks gold prices and emerging-market risk sentiment. When gold falls and global investors rotate into yield assets, ZAR weakens. This makes Dubai property purchases significantly more expensive for South African buyers in periods of risk-on sentiment.

USD — US Dollar. Pegged at 3.6725 AED. Effectively zero FX risk on Dubai property. American buyers focus only on the AED purchase price and timing of their property decision, not currency movements.

Want updated home-currency figures on a Dubai property you're considering? Our team can model FX impact across staged payments before you commit.

Request a Currency-Adjusted QuoteOff-Plan Staged Payments: Hidden FX Risk and How to Manage It

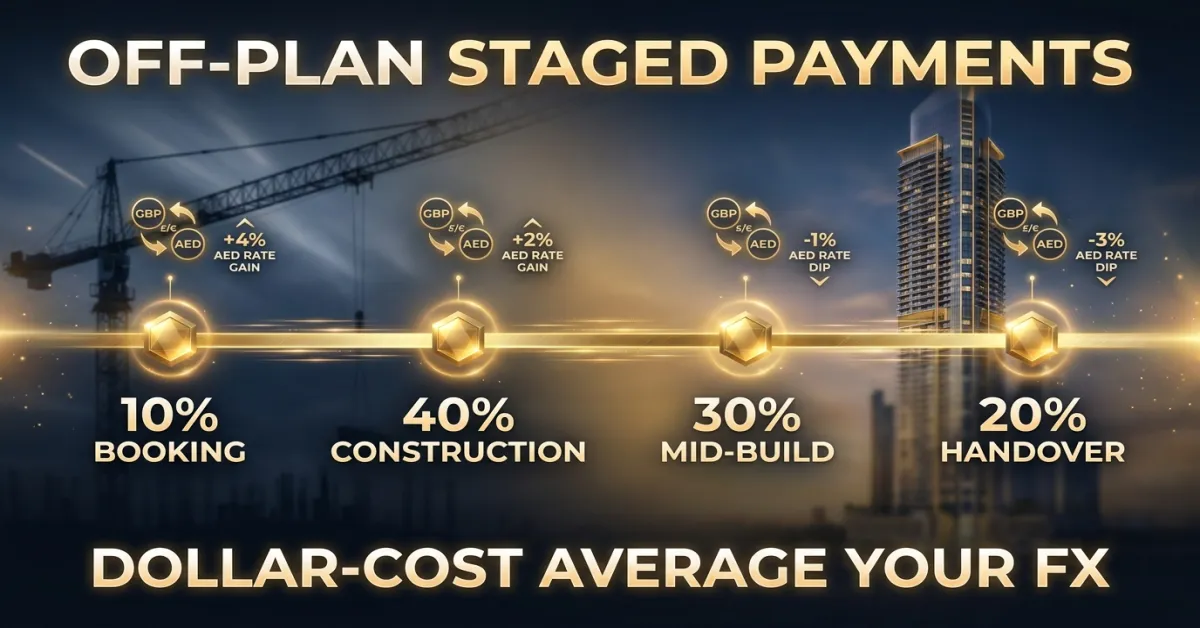

Most Dubai off-plan purchases use staged payment structures stretching over 2-4 years. Common ratios include 50/50, 60/40, 70/30, and 80/20, where the first number is the percentage paid during construction and the second is paid at handover. Some developers offer post-handover payment plans extending an additional 1-3 years.

For non-USD buyers, each unpaid installment is an open FX position. If your home currency weakens against AED before the next milestone, that installment becomes more expensive in your home currency. Over a typical 3-year off-plan timeline, cumulative FX swings of 5-15% are normal for GBP and EUR holders.

Strategy 1 — Front-load conversion. If today's exchange rate is favorable, convert the full purchase amount to AED and hold it in a UAE AED savings account. Locks in cost. Best when your home currency is at recent highs against AED.

Strategy 2 — Convert each installment separately. Provides natural dollar-cost averaging. You buy AED at multiple rates over the construction period, smoothing out volatility. Best when you do not have a strong directional view on your home currency.

Strategy 3 — Forward contracts via FX specialists. Lock in a future exchange rate today for a future payment date. Removes FX risk entirely on a specific installment. Specialists like Wise, OFX, TorFX, and Moneycorp typically charge spreads of 0.3-0.7%, compared to 2-4% at traditional high-street banks. On an AED 2 million transfer, this fee differential alone saves GBP 5,000-15,000.

Why Geopolitical Volatility Helps and Hurts Dubai Property Buyers

Global uncertainty — Iran tensions, central bank surprises, oil price spikes — creates short-term currency swings that can either reduce or increase your Dubai property cost depending on your home currency. The pattern in 2026 has been counter-intuitive in places.

The US dollar weakened slightly during recent geopolitical escalation despite the typical safe-haven flow into USD. Stronger US labour cost data shifted Federal Reserve rate expectations, contributing to USD softness. For non-USD buyers, USD weakness translates directly into cheaper AED purchases — a small but real window for European, UK, Canadian, and South African investors.

For Dubai property buyers, the implication is clear: short-term FX swings rarely move in a straight line, and the cost of a Dubai purchase in your home currency can shift several percentage points within a single quarter. A buyer who waits passively for "the right moment" usually loses to a buyer who has a structured FX plan tied to the developer's payment schedule.

For HNI investors targeting AED 2 million+ properties under the Dubai investor visa or Golden Visa, FX strategy is part of the residency strategy. A 5% FX swing on a AED 2 million purchase is AED 100,000 — enough to fund Emirates ID renewal cycles for several years.

Frequently Asked Questions

Is the AED really pegged to the USD?

Yes, the UAE Dirham has been pegged to the US Dollar at 1 USD = 3.6725 AED since November 1997. The Central Bank of the UAE intervenes automatically in foreign exchange markets to maintain this rate, backed by significant USD reserves. The peg is considered extremely stable and unlikely to break in 2026 or the foreseeable future.

How much can currency swings change my Dubai property cost?

For GBP and EUR buyers, 5-15% swings against AED over a typical 2-4 year off-plan payment timeline are normal. On an AED 3 million property, a 10% adverse FX move adds the equivalent of AED 300,000 to your home-currency cost without any change in the property's listed price. American buyers face zero FX risk thanks to the AED-USD peg.

Should I convert all my money to AED upfront or pay in installments?

Both work in different conditions. Front-loading conversion locks in cost at today's rate — ideal when your home currency is at recent highs against AED. Converting each installment separately provides dollar-cost averaging — ideal when you have no strong view on your currency's direction. Forward contracts via FX specialists let you lock specific future installments without converting today.

Are FX specialists really cheaper than my UK or EU bank?

Yes, typically by a wide margin. FX specialists like Wise, OFX, TorFX, and Moneycorp charge spreads of 0.3-0.7%, while traditional high-street banks charge 2-4%. On an AED 2 million transfer, the fee differential alone is GBP 5,000-15,000. Most also offer forward contracts that banks do not provide to retail customers.

Does the AED move at all against the US dollar?

No, not in any meaningful way. The peg holds 1 USD = 3.6725 AED with very narrow daily fluctuations of fractions of a percent. For US-dollar-denominated buyers, the AED price you agree on today is effectively the USD price you will pay across the entire transaction.

How do I plan FX timing for an off-plan purchase with a 60/40 payment plan?

Map each developer milestone to a corresponding FX action. For booking and early construction installments, evaluate today's rate against your historical average. For later milestones, consider forward contracts to lock the rate in advance. A staged FX plan tied to your payment schedule typically saves 3-7% versus converting reactively at each milestone.

Muhammad Zohaib

Founder & CEO of Early Bird Properties with 13+ years of Dubai real estate experience. RERA certified.