Dubai Property for UK Non-Doms: A 2026 Investor Guide After Tax Abolition

As of Q1 2026, 16,500 UK millionaires left Britain for destinations like Dubai in 2025 alone — more than double 2024's 7,500 outflow — following the April 2025 abolition of non-dom status that lifts UK income tax exposure to 47% from 2027 (Henley & Partners, 2025). According to Early Bird Properties' transaction data, UK buyer enquiries on Dubai villas rose sharply through Q4 2025, concentrated in Dubai Hills, Palm Jumeirah and Emirates Hills. This guide explains exactly how a UK non-dom buys Dubai property in 2026 — the tax mechanics under the UK-UAE Double Taxation Agreement, the AED 2 million Golden Visa pathway, the best communities by yield, and a 90-day relocation playbook tested on real client moves.

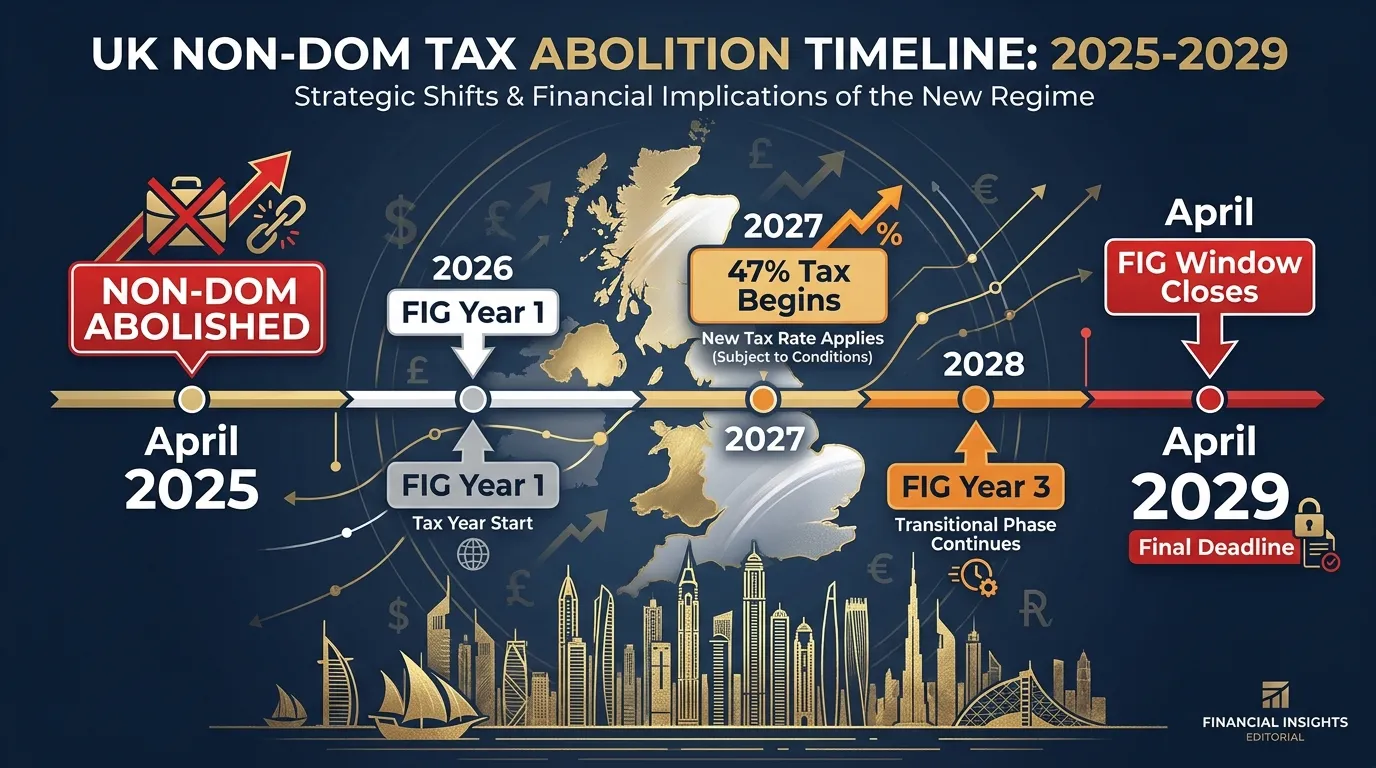

What the April 2025 UK Non-Dom Abolition Means for Property Investors

The UK non-domiciled tax regime, in place since 1799, was abolished on 6 April 2025. The remittance basis — which let non-doms shelter foreign income and gains from UK tax for up to 15 years — has been replaced by a four-year Foreign Income and Gains (FIG) transition. After year four, worldwide income becomes taxable at UK rates, and worldwide assets fall into the UK 40% inheritance tax net.

The numbers are stark. UK additional rate income tax stands at 45%, rising effectively to 47% from 2027 once the National Insurance overlay is included (HMRC, 2025). Capital gains on residential property are charged up to 24%. Inheritance tax claims 40% of estates above £325,000. For a UK-resident non-dom holding international wealth, the post-2027 effective tax rate often exceeds 50% across income, gains and estate.

Dubai charges 0% personal income tax, 0% capital gains tax, 0% inheritance tax, and 0% tax on rental income. The mathematical case for relocating wealth and residency has never been clearer — and the property market is where most UK non-doms anchor that move, because Dubai property ownership unlocks the 10-year Golden Visa.

Why 16,500 UK Millionaires Are Choosing Dubai in 2025-2026

Henley & Partners' 2025 Wealth Migration Report recorded 16,500 high-net-worth individuals leaving the UK in 2025 — 120% above 2024's 7,500 figure and the largest single-year millionaire outflow from any G7 country in recent records. The UAE was the world's top destination, absorbing roughly 9,800 millionaires in the same period. A Hubbis Wealth Management survey published in Q1 2026 found 71.6% of UK wealth managers reported increased client enquiries about relocation in the prior six months.

Dubai's pull goes beyond tax. As of Q1 2026, the emirate recorded AED 252 billion in property transactions across 60,303 deals, a 31% year-on-year increase (Dubai Land Department / Dubai Media Office, Q1 2026). Foreign investment alone reached AED 148.35 billion across 29,312 new investors, up 26% YoY. The luxury segment — homes above AED 10 million — settled AED 87.71 billion, also +26% YoY. Knight Frank's 2025 Wealth Report shows Dubai prime residential prices up 193.9% over five years and +25.1% YoY, the strongest performance of any prime city worldwide.

For UK non-doms, three structural factors matter most: the AED 2 million Golden Visa anchors a 10-year residency without renewal headaches; the AED-USD peg (3.673) eliminates currency risk versus dollar-denominated assets; and English-language conveyancing under DLD oversight makes the buying process faster than London. Browse current inventory at /buy or /off-plan-properties.

UK-UAE Double Taxation Agreement Explained in Plain English

The UK-UAE Double Taxation Agreement (DTA) was signed in 2016 and has been in force ever since (HMRC, UAE Ministry of Finance). Its purpose is simple: prevent the same income from being taxed twice. For UK non-doms relocating to Dubai, three articles do the heavy lifting.

Article 6 (Income from Immovable Property) allocates exclusive taxing rights on rental income to the country where the property sits. Dubai rental income is therefore taxable only in the UAE — which charges 0% — provided you are non-UK-resident under the Statutory Residence Test (SRT). Article 13 (Capital Gains) gives the UAE exclusive taxing rights on gains from Dubai property disposals. Article 4 (Residence) and the tie-breaker rules determine where you are treated as resident when both countries claim you, with permanent home, centre of vital interests and habitual abode tested in order.

The catch: the DTA only protects you if you are genuinely non-UK-resident under the SRT. Failing the SRT — typically by spending too many days in the UK or retaining too many "ties" — collapses the protection and brings worldwide income back into UK tax. This is why the SRT day-count strategy matters more than any tax structuring.

Planning a UK exit before April 2027? Speak to a RERA-certified adviser who has handled 50+ UK non-dom relocations.

Speak to a Dubai Adviser

Tax Savings Worked Example: £2M UK Buyer to Dubai

A £2 million GBP allocation converts to roughly AED 9.2 million at 4.6 AED to the pound. The structure used most often by Early Bird Properties' UK clients splits this two ways: a primary residence that triggers the Golden Visa, and a yield-stack of smaller apartments that generates retained tax-free income.

Allocation A — AED 5.5 million Dubai Hills Estate four-bedroom villa. This becomes the UAE primary residence, satisfies the AED 2 million Golden Visa threshold (with a buffer for any future price softening), and qualifies the spouse and children as dependants on the same visa. Estimated rental yield if leased: AED 275,000 per year at 5.0% gross.

Allocation B — AED 3.6 million spread across four JVC one-bedroom apartments at AED 900,000 each. Bayut's 2025 rental data places JVC one-bed gross yields at 7.04% as of late 2025, with studios at 7.87%. Four units at AED 70,000 annual rent each generate AED 280,000 — a working yield engine.

Combined gross rental: AED 555,000 per year if the villa is rented, or AED 280,000 if owner-occupied. Compare to the UK alternative: a £2 million buy-to-let portfolio in London yielding 4% gross would produce £80,000, taxed at 45% income plus 5% surcharge SDLT on purchase, leaving £44,000 net. The Dubai owner-occupied case retains AED 280,000 — roughly £61,000 — fully tax-free, while also extinguishing UK CGT and IHT exposure on those assets.

AED 2M Golden Visa Pathway for UK Non-Doms

The Dubai Golden Visa for property investors is set at AED 2 million minimum since the 2022 reform that removed the previous AED 750,000 threshold. The visa is renewable for 10 years, includes spouse and children as dependants with no age cap, and permits unlimited entry/exit without losing residency status (UAE General Directorate of Residency).

Eligibility rules UK buyers commonly miss: the AED 2 million can sit across multiple properties (so two AED 1 million apartments work) provided each is registered in your sole name; off-plan property qualifies once 50% of the purchase price has been paid to a developer escrow account; mortgage-financed properties qualify, but only the equity portion counts toward the AED 2 million threshold. Holding the property throughout the 10-year visa term is mandatory — a sale terminates the visa unless replaced.

Processing timelines as of Q1 2026 average 14-21 working days from DLD title transfer to visa stamping. Total government and medical fees fall in the AED 9,000-12,000 range. The visa unlocks UAE bank account opening, Emirates ID, school enrolment for children, and — critically for UK non-doms — a UAE tax residency certificate, which is the document HMRC uses when reviewing SRT challenges. See full advisory support at /services.

Best Dubai Communities for UK Non-Dom Buyers

UK non-dom buyers cluster in five communities, each serving a different mandate. Selection should follow the wealth strategy — prestige, family lifestyle, yield, or capital preservation — not generic "best area" lists.

Palm Jumeirah — 5.5% yield, prestige + tourism

The signature address of Dubai. Apartments from AED 3 million, signature villas from AED 25 million. Strong short-let rental performance through DET-licensed holiday lets. Best for buyers who value brand recognition and tourism-driven income on top of the residential yield.

Dubai Hills Estate — 5.0% yield, family villas + schools

The mandatory shortlist for UK families relocating with school-age children. GEMS, Kings' and other British curriculum schools sit inside or adjacent to the community. Four-bed villas trade in the AED 4.5-7 million range. Lower yield reflects lifestyle premium and stronger capital growth profile.

Emirates Hills — 4.0% yield, ultra-prime

Dubai's "Beverly Hills". Mansions from AED 35 million to AED 200 million+. The yield is intentionally low — buyers here prioritise capital preservation and peer-group address quality. Times and Telegraph readers who valued The Bishops Avenue or Holland Park typically settle here.

JVC (Jumeirah Village Circle) — 7.5% yield, the yield engine

Not a residence community for HNW UK buyers — a yield play to allocate alongside the primary residence. AED 900K-1.4M one-beds let at the highest gross yields in mainstream Dubai. Bayut data shows 7.04% on one-beds, 7.87% on studios as of late 2025. Used by 80% of Early Bird's UK clients as the income leg.

District One — capital preservation

Mohammed Bin Rashid City's villa cluster around Crystal Lagoon. AED 12-50 million villas. Tight supply, restrictive resale (no flips for first 18 months), and strong off-plan-to-handover appreciation. The capital-preservation pick for buyers planning a 10-15 year hold.

Mortgage Mechanics for UK Non-Doms in 2026

UAE Central Bank rules cap loan-to-value for non-residents at 50% on properties under AED 5 million and 40% on properties above. UK income is acceptable for affordability if the borrower's UK tax returns and three months of bank statements support the debt service. Typical interest rates as of Q1 2026 sit at 4.25-4.75% on UAE-based mortgages — a non-trivial premium over UK rates, but tax-deductible against UAE rental income (which is taxed at 0%, so the deduction is moot).

A common UK non-dom mistake: arranging a UK-pound mortgage against UK assets to fund the Dubai purchase. This works financially but creates SRT complexity — the borrowing structure can imply continued UK economic ties. Most clients use a UAE-side mortgage in their own name, or buy outright if the cash position allows. Buying outright simplifies the SRT defence.

Off-Plan vs Ready Stock — 2026 Strategy

As of Q1 2026, 67% of new transactions in Dubai were off-plan, with the balance in ready stock (DLD Q1 2026 data). The choice for UK non-doms hinges on the relocation timeline.

If you need residence within 12 months — ready stock. Title transfers in 7-14 days, the Golden Visa is processable inside three weeks, and you can break UK residence cleanly in the same tax year. Premium of 10-15% over equivalent off-plan, but the timeline certainty is decisive.

If your UK exit is 24-36 months away — off-plan with 30-50% during construction and balance on handover. This staged approach matches the FIG transition timeline, captures developer launch pricing typically 15-25% below ready market, and uses the construction window to organise the personal move. Browse vetted launches at /off-plan-properties.

First 90 Days in Dubai — Relocation Playbook

Days 1-30: arrive on visit visa, complete property purchase if not already done, file Golden Visa application immediately on title transfer, open UAE bank account (Emirates NBD or HSBC UAE accept Golden Visa applicants pre-issuance with property title deed), enrol children in school for the next admission cycle.

Days 31-60: Emirates ID issued, apply for UAE driving licence (UK licence converts directly), register with UAE tax authority for the tax residency certificate (issued after 183 days of physical presence), establish "centre of vital interests" markers — gym membership, doctor, accountant, family physician on UAE addresses.

Days 61-90: review SRT day-count for the UK tax year, document UK tie reductions in writing (work, accommodation, family, 90-day, country ties), engage a UK-side tax adviser to prepare the split-year treatment claim if mid-year departure, and lodge the formal HMRC P85 if not already submitted. By day 90, the UAE residence claim should be defensible against any SRT challenge.

Frequently Asked Questions — UK Non-Doms Buying Dubai Property

Do I have to leave the UK to buy Dubai property as a non-dom?

No. UK residents can buy Dubai property. But to access UAE 0% tax on rental income, you must break UK residence under the Statutory Residence Test — typically <90 days in UK and severing housing/work/family ties.

What is the Dubai Golden Visa minimum property investment in 2026?

AED 2 million for the 10-year renewable Golden Visa. The earlier AED 750K threshold was removed. Spouse and children qualify as dependants. Property must be held throughout the visa period.

Will I pay UK capital gains tax on my Dubai property?

If you have established non-UK residence under the SRT before sale, no UK CGT applies on Dubai property gains. UAE charges 0% capital gains tax. The UK-UAE DTA allocates exclusive taxing rights to the UAE for the property's location.

Which Dubai community has the best rental yield for UK buyers in 2026?

Jumeirah Village Circle (JVC) leads at ~7.5% gross yield as of early 2026, per Bayut data. Dubai Hills villas yield ~5%. Emirates Hills and Palm Jumeirah deliver 4-5.5% with stronger capital appreciation.

How much UK income tax will I pay if I stay after April 2025?

Up to 45% additional rate (47% including National Insurance from 2027) on worldwide income, plus 40% inheritance tax on worldwide assets after a 4-year FIG transition. Dubai charges 0% on the same income.

Can I keep my UK home while moving to Dubai?

Yes, but it counts as a UK "tie" under the SRT. You must combine it with limited UK days and other tie reductions. Many UK non-doms rent the UK home rather than sell, but tax advice is essential before establishing the day-counting strategy.

What is the UK-UAE Double Taxation Agreement and how does it help me?

Signed in 2016, in force ever since. The DTA prevents the same income being taxed by both UK and UAE. For Dubai-sourced rental and property gains, taxing rights sit with the UAE — which charges 0% — provided you are non-UK-resident under the SRT.

The 2026 Window for UK Non-Dom Buyers

The four-year FIG transition that began April 2025 ends April 2029. Every month inside that window is a month of optionality — break UK residence cleanly, anchor the Dubai Golden Visa on AED 2 million of property, and the UK-UAE DTA does the rest. Dubai prime is up 193.9% over five years, off a market that is still nearly 30% below 2014 inflation-adjusted peaks. The combination of forced UK migration, AED-USD peg stability, and 0% personal tax is unlikely to repeat in the next decade.

Muhammad Zohaib

Founder & CEO of Early Bird Properties with 13+ years of Dubai real estate experience. RERA certified.