DLD Transactions Q1 vs Q2 2026: What Changed in Dubai's Market

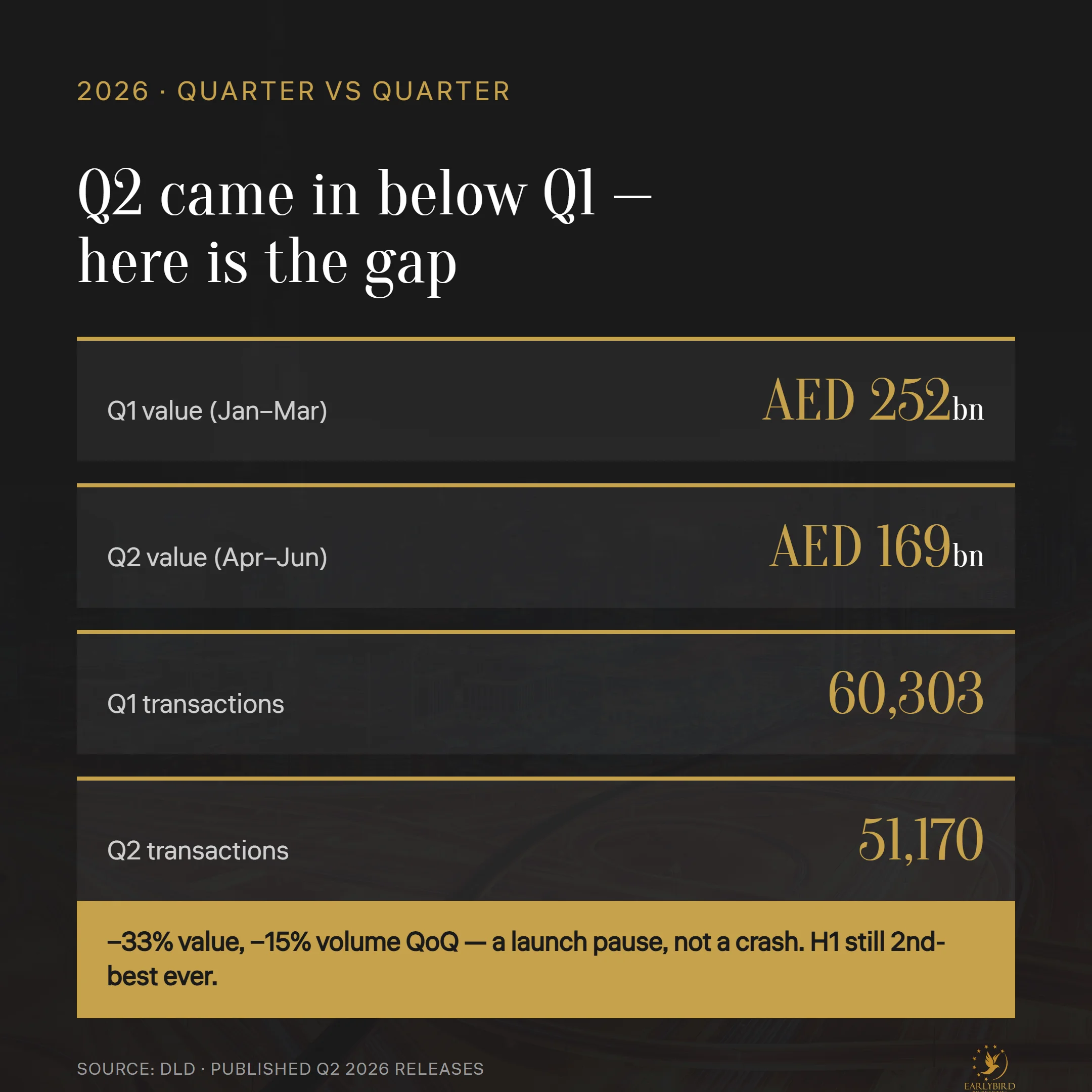

Dubai's first quarter of 2026 recorded AED 252 billion across 60,303 DLD transactions; the second quarter came in at AED 169.04 billion across 51,170. That is a 33 percent drop in value and 15 percent in volume quarter on quarter — yet the half still closed at 86,005 sales worth AED 286.43 billion, the second-highest H1 in Dubai's history, and off-plan held roughly 74 percent of residential sales throughout. This comparison walks the official record quarter against quarter: what actually fell, what held, and our broker-side read — labelled as opinion — on what it sets up for the third quarter.

All aggregates are DLD figures from published quarterly and half-year releases; derived percentages are flagged as derived. This is data reporting, not a forecast.

The two quarters side by side

Value -33%, volume -15% quarter on quarter

| Metric | Q1 2026 | Q2 2026 | Change (derived) |

|---|---|---|---|

| Total value | AED 252bn | AED 169.04bn | -33% |

| Transactions | 60,303 | 51,170 | -15% |

| Value per deal (derived) | ~AED 4.18M | ~AED 3.30M | -21% |

Q2 detail the Q1 release did not carry: mortgages AED 42.6 billion across 10,522 deals, gifts AED 16 billion across 2,449. The falling value-per-deal is itself a signal — our read, labelled as opinion: Q1 carried an unusual weight of high-value and luxury activity (AED 87.71 billion in the luxury segment alone), and Q2 rebalanced toward mid-market volume.

Why Q2 came in lower

Three drivers, in order of evidence. First, the launch calendar: new project launches concentrated into January and February, then paused from March — Savills flagged in advance that off-plan volumes would ease in Q2 for exactly this reason. Second, May: both volumes and values recorded a notable dip mid-quarter, with the ready market slowing hardest. Third, seasonality — Q2 runs into summer and, in 2026, through Ramadan-adjacent scheduling that pushed developer activity earlier.

What it is not, labelled as our opinion: a demand collapse. H1 2026 launches totalled AED 275 billion in announced project value — the largest first-half development cycle on record — and developers do not commit that scale into a market they believe is rolling over. The wider bubble question is covered in our Dubai property bubble analysis.

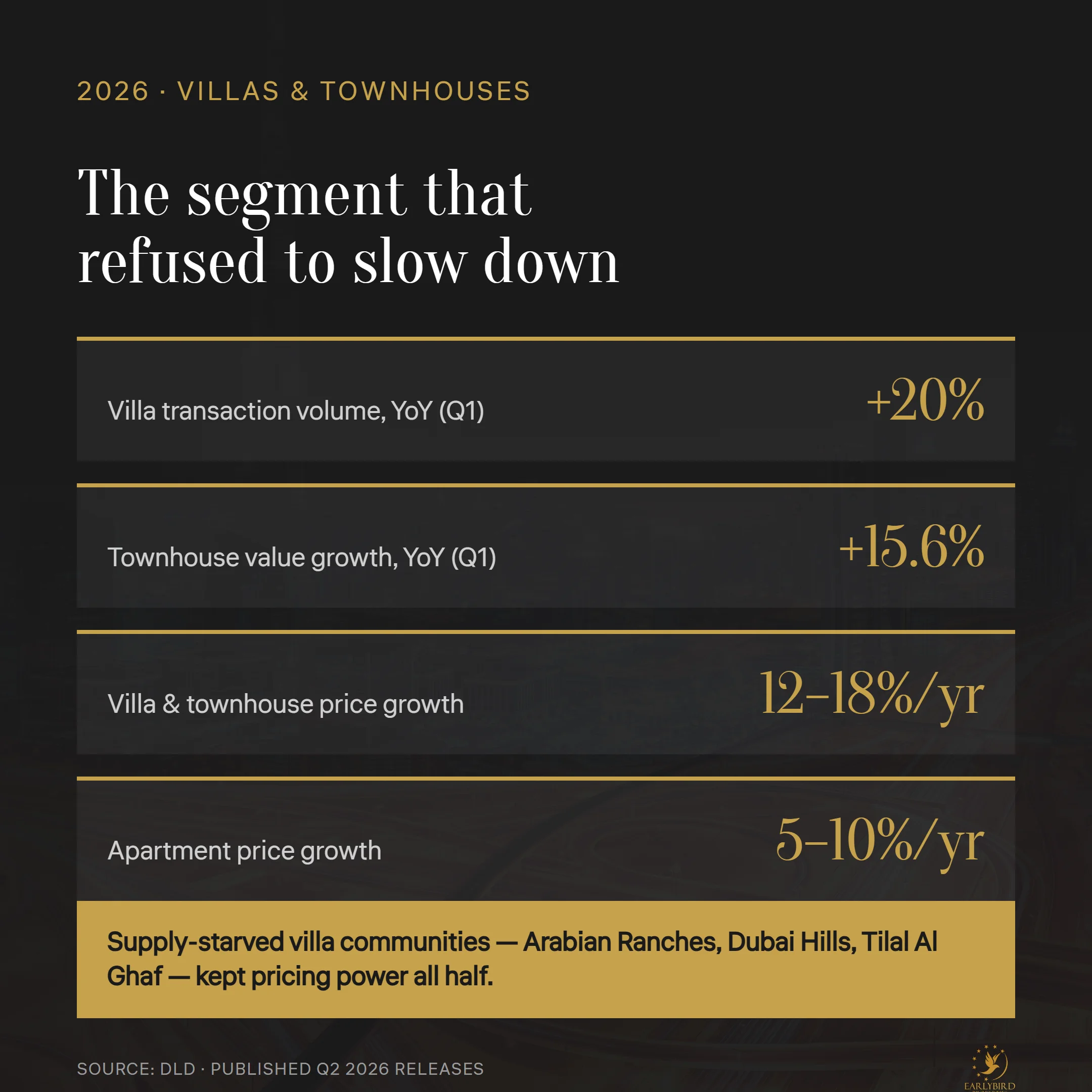

What held: off-plan share, villas and townhouses

Villas and townhouses kept pricing power through both quarters

Two things did not move. Off-plan's share of residential sales held near 74 percent in both quarters — the mix stayed constant even as absolute volume fell. And the villa-townhouse segment kept its pricing power: villa volumes up 20 percent year on year, townhouse value up 15.6 percent (Q1 reading, labelled), with villa and townhouse prices compounding at 12-18 percent annually against 5-10 percent for apartments. The full quarter picture is in our Q2 2026 market report.

H1 2026 in total

The half closed at 86,005 sales worth AED 286.43 billion — second only to H1 2025's AED 326.6 billion — spanning 71,570 residential units, 7,301 buildings and 7,134 land parcels. Counting all transaction types (sales plus mortgages, gifts and other registrations), H1 reached approximately AED 420 billion across 112,850 transactions. Foreign investment in Q1 alone was AED 148.35 billion with roughly 30,000 new foreign investors entering.

What to watch in Q3

Our read, labelled as opinion: the launch pipeline restarts. With AED 275 billion of H1-announced projects moving to sales phases and the autumn selling season ahead, Q3 volume should recover toward Q1's run-rate — the question is whether ready-market pricing firms with it. Watch the DLD official Q2 release later in July for the per-segment off-plan/ready split, which is not yet published; we will update against it. If the market's resilience thesis matters to your decision, start with why Dubai real estate didn't crash in 2026 and the Q1 2026 market report this comparison builds on.

Frequently asked questions

Why did Dubai transactions fall from Q1 to Q2 2026?

Mainly the launch calendar: new projects concentrated into January-February then paused from March, thinning fresh off-plan inventory through spring. A May dip in volumes and values — hitting ready stock hardest — plus summer seasonality did the rest. Value fell 33 percent, volume 15 percent quarter on quarter.

Was Q2 2026 a bad quarter for Dubai real estate?

No — it was a lower quarter, not a bad one. AED 169 billion across 51,170 transactions would have ranked among the strongest quarters of any prior year, and H1 2026 overall was the second-highest half-year on record at AED 286.43 billion in sales.

How much was Dubai's H1 2026 real estate market worth?

H1 2026 closed at 86,005 sales worth AED 286.43 billion — 71,570 residential units, 7,301 buildings and 7,134 land parcels. Counting every transaction type including mortgages and gifts, the half reached approximately AED 420 billion across 112,850 registrations, per DLD published figures.

Did off-plan lose market share in Q2 2026?

No. Off-plan's share of residential sales held near 74 percent through both quarters — absolute volumes eased with the launch pause, but the market mix did not shift toward ready stock. Within off-plan value, apartments took 81 percent and villas 11.3 percent.

Should buyers wait for Q3 2026 to purchase in Dubai?

Waiting trades today's negotiating room for tomorrow's fresh supply. Our labelled opinion: ready-market softness in Q2 favours buyers negotiating now, while off-plan buyers gain from the AED 275 billion H1 launch pipeline reaching sales phases in Q3. The right timing depends on your segment, not the headline.

Ask us about the quarter-on-quarter data - WhatsApp

Muhammad Zohaib Saleem — Founder, Early Bird Properties (RERA / DLD ORN 37167). In Dubai real estate since 2013.

Muhammad Zohaib Saleem — Founder, Early Bird Properties (RERA / DLD ORN 37167). In Dubai real estate since 2013.

Methodology & disclosure: market aggregates are Dubai Land Department figures as carried in published Q2 and H1 2026 releases (DLD half-year statement as reported by Economy Middle East and Arabian Business; Cavendish Maxwell; Savills; Dubai Chronicle). Figures covering a different period (Q1 or H1 2026) are labelled as such; derived figures are flagged as derived. The exact per-segment off-plan/ready count table for Q2 is not yet published by DLD and is therefore not claimed here. No developer marketing fees influence this analysis; recommendations are based solely on alignment with buyer and seller interest. This is data reporting, not investment advice.